Futures Market: Overnight, LME copper opened at $9,158.5/mt, with its center of gravity initially sinking during fluctuations, bottoming at $9,124/mt. It then climbed steadily, peaking at $9,292/mt near the session's end and closing at $9,270/mt, up 1.05%. Trading volume reached 21,000 lots, and open interest stood at 280,000 lots. Overnight, the most-traded SHFE copper 2503 contract opened at 75,080 yuan/mt, with its center of gravity slightly declining initially and bottoming at 74,840 yuan/mt. It then fluctuated upward, peaking at 75,780 yuan/mt near the session's end and closing at 75,730 yuan/mt, up 0.56%. Trading volume reached 30,000 lots, and open interest stood at 157,000 lots.

【SMM Copper Morning Brief】News: (1) The US January ISM Non-Manufacturing PMI recorded 52.8, significantly below expectations, while January ADP employment increased by 183,000, marking the highest level since October last year.

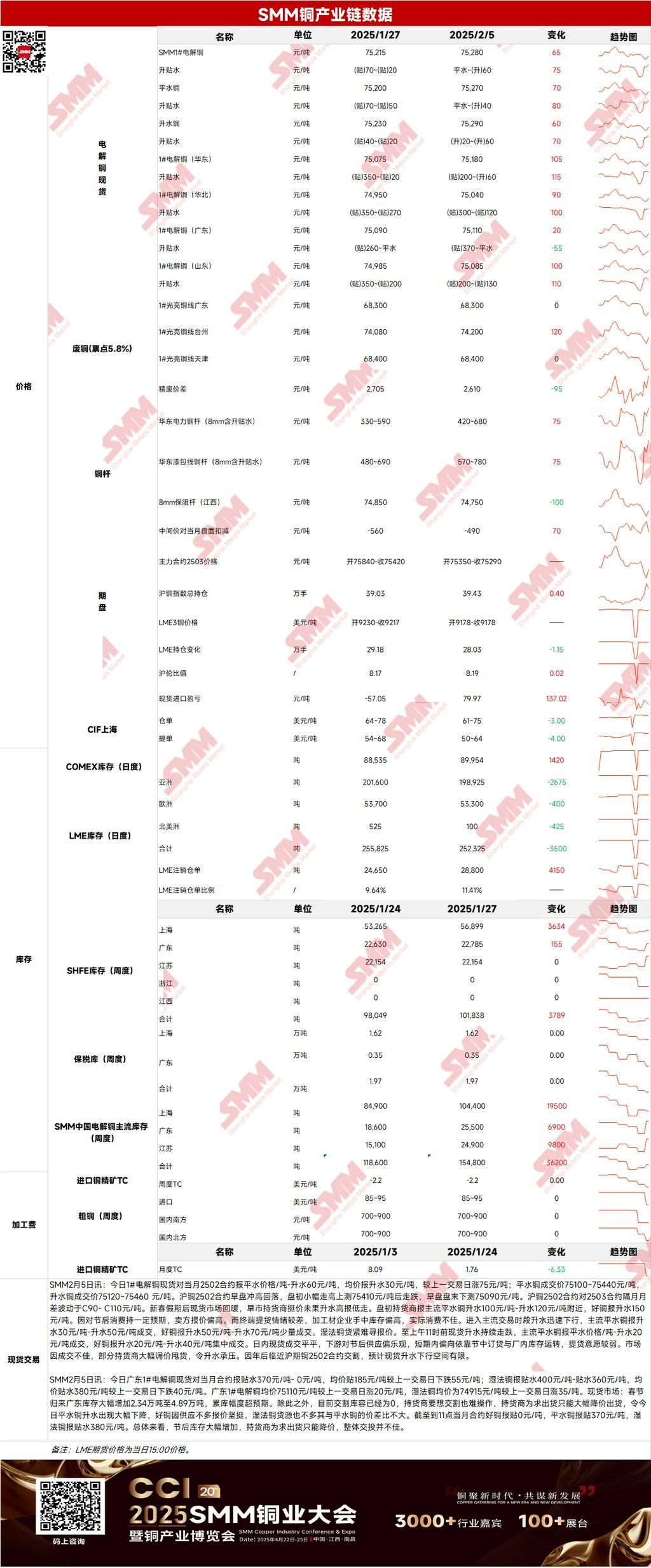

Spot Market: (1) Shanghai: On February 5, mainstream standard-quality copper spot prices against the front-month contract were quoted at parity to premiums of 40 yuan/mt, while high-quality copper was quoted at premiums of 20-60 yuan/mt. Spot transactions were mediocre during the day, as downstream players remained optimistic about post-holiday supply and preferred to rely on holiday orders and in-plant inventory for operations in the short term, showing weak willingness to pick up goods. Due to poor transactions, some suppliers significantly adjusted prices to offload goods, putting pressure on premiums. With the SHFE copper 2502 contract nearing delivery, spot premiums are expected to have limited downside room.

(2) Guangdong: On February 5, Guangdong #1 copper cathode spot prices against the front-month contract were quoted at discounts of 370 yuan/mt to parity, with an average discount of 185 yuan/mt, down 55 yuan/mt from the previous trading day. Hydro copper was quoted at discounts of 400-360 yuan/mt, with an average discount of 380 yuan/mt, down 40 yuan/mt from the previous trading day. The average price of Guangdong #1 copper cathode was 75,110 yuan/mt, up 20 yuan/mt from the previous trading day, while hydro copper averaged 74,915 yuan/mt, up 35 yuan/mt. Overall, post-holiday inventories increased significantly, forcing suppliers to lower prices to promote sales, resulting in lackluster overall transactions.

(3) Imported Copper: On February 5, warehouse warrant prices ranged from $61 to $75/mt, QP February, with an average price down $3/mt from the previous trading day. B/L prices ranged from $50 to $64/mt, QP February, with an average price down $3/mt from the previous trading day. EQ copper (CIF B/L) was quoted at $3-17/mt, QP February, with the average price unchanged from the previous trading day. Quotes referenced cargoes arriving in mid-to-early February. Post-holiday SHFE/LME price ratio improved significantly compared to pre-holiday levels, but buying activity was subdued on the first trading day. Scattered offers for pyrometallurgical copper arriving in mid-to-early February were observed, while EQ supply remained tight. Most traders adopted a wait-and-see attitude toward the market, with the overall transaction center shifting downward.

(4) Secondary Copper: On February 5, secondary copper raw material prices remained unchanged MoM. Guangdong bare bright copper prices were 68,200-68,400 yuan/mt, unchanged MoM. The price difference between primary metal and scrap was 2,610 yuan/mt, down 95 yuan/mt MoM. The price difference between primary and secondary copper rods was 1,040 yuan/mt. According to the SMM survey, on the first trading day after the holiday, copper prices showed little fluctuation, downstream restocking willingness was moderate, and secondary copper rod enterprises reported decent performance in new orders.

(5) Inventory: On February 5, LME copper cathode inventory decreased by 2,625 mt to 252,325 mt. On the same day, SHFE warehouse warrant inventory increased by 1,014 mt to 26,459 mt.

Prices: Macro-wise, the US January ISM Non-Manufacturing PMI recorded 52.8, significantly below expectations, while January ADP employment increased by 183,000, marking the highest level since October last year. US data showed mixed results, with the US dollar index continuing to decline and fluctuating at low levels, providing support for copper prices. On the fundamentals side, on the first trading day after the holiday, spot transactions were mediocre, with most downstream copper rod plants still holding ample inventories and showing weak willingness to pick up goods. Overall transactions were poor, and many downstream enterprises are expected to resume operations around the Lantern Festival. The market is still awaiting recovery. In summary, post-holiday consumption has not fully recovered, and copper prices are expected to lack sustained upward momentum today.

》Click to view the SMM Metal Database

【The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided herein is for reference only and does not constitute direct investment research advice. Clients should make prudent decisions and not substitute this for independent judgment. Any decisions made by clients are unrelated to SMM.】